The Complete Guide to Buying Your First Home in 2026

Apr 02, 2026

Written by David Dodge

Rates have eased, inventory is rising, and buyers have more leverage than in years. Here's exactly what to do — step by step.

Buying a home is one of the biggest financial moves you'll ever make — and right now in 2026, the landscape is finally shifting in buyers' favor. Mortgage rates have pulled back from their 2023 peak of above 7%, inventory is climbing in most markets, and sellers are becoming more willing to negotiate. But the process itself? Still complex, full of jargon, and easy to get wrong if you don't know what to expect.

This guide walks you through every stage — from checking your finances to getting your keys — in plain English. No fluff, no scare tactics. Just the facts you need to move forward with confidence.

01. The 2026 Housing Market at a Glance

Before you start looking at houses, it's worth understanding the environment you're stepping into. The market today is dramatically different from the frenzied seller's market of 2021–2022, and even from the frozen, rate-shocked market of 2023. Here's what the numbers look like right now:

30-Yr Fixed Rate

6.38%

As of Mar 26, 2026

15-Yr Fixed Rate

5.75%

↓ From 5.89% last year

Projected Growth

~2%

↑ Slower than prior years

Market Balance

Near even

Most balanced in a decade

30-Year Fixed Mortgage Rate: 2020–2026

Source: Freddie Mac Primary Mortgage Market Survey

According to Freddie Mac, the 30-year fixed mortgage rate averaged 6.38% for the week ending March 26, 2026 — up slightly from the prior week but still lower than the 6.65% seen a year ago. The 15-year fixed rate came in at 5.75%.

NAR's leading economists note that this will likely be the first year since 2020 where monthly mortgage payments actually decline year-over-year — a meaningful milestone for buyers who've been waiting on the sidelines.

⚠️ Important Context

Even at 6.38%, today's rates are well below the long-term historical average of ~7.8% going back to 1971. If you're waiting for rates to return to 2021's record lows of 2–3%, most economists agree that's extremely unlikely in any near-term scenario.

Wells Fargo projects the 30-year fixed rate to average around 6.14% for all of 2026, with most major institutions forecasting rates to stay in the low-to-mid-6% range throughout the year. J.P. Morgan Research expects home prices to essentially stall nationally in 2026, with regional variation, which means you won't be racing against rapid appreciation in most markets.

💡 First-Timer Tip

A rate of 6.38% sounds high compared to what you may have heard about in 2020–2021. But consider this: on a $300,000 loan, the difference between 6.38% and 7% is about $120/month. That's significant, but the bigger lever is the home price itself — negotiate hard there.

02. Getting Your Finances in Order First

Before you even browse a single listing, you need an honest picture of your financial health. Lenders will look at several key numbers, and so should you. This is where most first-time buyers underestimate the preparation required.

Know Your Credit Score

Your credit score is one of the most important factors in determining what mortgage rate you'll qualify for — potentially saving or costing you tens of thousands of dollars over the life of the loan. Here's a rough breakdown:

Pull your free credit report from AnnualCreditReport.com and check for errors. Disputing inaccurate negative items can meaningfully boost your score before you apply.

Your Debt-to-Income Ratio (DTI)

Lenders don't just look at your income — they look at how much of it is already spoken for by debt. Your debt-to-income ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI below 43%, with the best rates going to borrowers under 36%.

📊 Example

If your gross monthly income is $6,000 and you pay $400/month in student loans and $200 in car payments, your existing DTI is 10%. Add a projected $1,500 mortgage payment, and your total DTI becomes 35% — comfortably within most lenders' requirements.

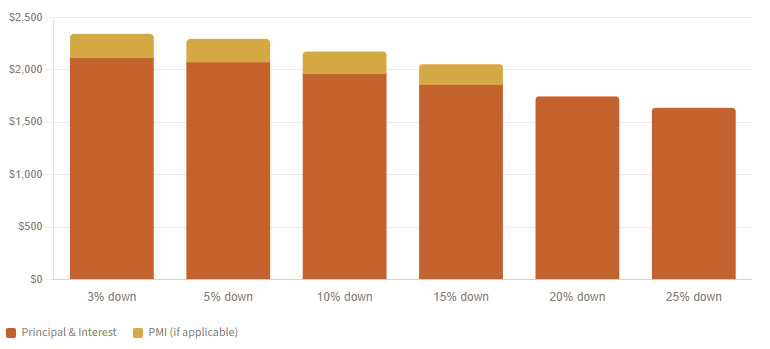

How Much Do You Actually Need to Save?

This is the question that stops most first-time buyers in their tracks. The answer is more nuanced than "20% down." Here's what you actually need to prepare for:

According to NAR research, first-time buyers in 2026 are putting down an average of 10% — the highest in nearly 40 years — largely because rising home prices require a larger absolute dollar amount even for the same percentage. Many buyers are living with family or pooling resources to hit that threshold.

Monthly Payment by Down Payment Amount

Based on a $350,000 home at 6.38% interest rate (30-year fixed). PMI is estimated at 0.8% for loans below 20% down.

💡 First-Timer Tip

NAR's research shows there are many assistance programs most buyers don't know about — from state-level down payment assistance to employer homebuying benefits. Always ask your lender specifically about first-time buyer programs before assuming you need a large down payment.

03. Getting Pre-Approved for a Mortgage

Pre-approval is not the same as pre-qualification. Pre-qualification is a rough estimate based on self-reported information. Pre-approval is a formal process where a lender reviews your actual financial documents and commits to lending you a specific amount at a specific rate — conditionally. It carries real weight with sellers.

What You'll Need to Gather

- Last two years of federal tax returns (W-2s or 1099s if self-employed)

- Recent pay stubs (last 30 days)

- Last two months of bank and investment account statements

- Government-issued ID and Social Security number

- Information on any existing debts (student loans, car payments, credit cards)

- Rental history (if you don't currently own)

Shop Multiple Lenders — This Is Critical

Most first-time buyers accept the first rate they're offered. Don't. According to The Mortgage Reports, borrowers who get at least three quotes save an average of $1,500 in the first year alone. Even a 0.25% difference on a 30-year loan can mean over $15,000 in total interest.

Compare quotes from at least three of these types of lenders:

A — Big Banks

Familiar brands, multiple products, but not always the most competitive rates. Good for existing customers who may get loyalty discounts.

B — Credit Unions

Often have lower rates than banks and more personalized service. Membership requirements usually aren't difficult to meet.

C — Mortgage Brokers

Shop your application across dozens of lenders simultaneously. Great for people with complex financial situations or who want someone to do the comparison shopping for them.

D — Online Lenders

Fastest pre-approval process, often with competitive rates, but less personal guidance. Best for tech-comfortable buyers with straightforward financial profiles.

Understanding Adjustable-Rate Mortgages (ARMs) in 2026

With fixed rates in the mid-6% range, more buyers are exploring ARMs. Bank of America reports that roughly 10% of its current loan volume is ARMs — the highest share since 2023. A 5/1 ARM typically offers a rate 0.5–1.5% lower than a 30-year fixed for the first five years, then adjusts annually. This can make sense if you plan to sell or refinance before the adjustment period kicks in.

04. Finding the Right Home in Today's Market

With your pre-approval in hand, you're now a serious buyer. Here's how to search smartly in the 2026 market.

Find a Real Estate Agent — Even in a Digital World

In the age of Zillow and Redfin, you might wonder if you need an agent. The answer for first-time buyers is almost always yes. An experienced buyer's agent costs you nothing (seller typically pays both agents' commissions), can alert you to listings before they hit public sites, helps you craft competitive offers, and guides you through inspections and negotiations. Interview at least two or three agents before committing.

What the 2026 Market Actually Feels Like

NAR economists describe the 2026 market as "the most balanced in nearly a decade." That means:

- Less frenzied bidding wars. Unlike 2021, you won't necessarily need to offer 10–15% over asking with no contingencies just to compete.

- More inventory than in recent years. Listings are up year-over-year in most metros, giving you more to choose from.

- Seller concessions are back. Many sellers are now offering closing cost credits, rate buydowns, or price reductions — especially on homes sitting for 30+ days.

- Builder incentives on new construction. Homebuilders are offering mortgage rate buydowns of 100–200 basis points below market rates, per J.P. Morgan.

Evaluate Each Home Carefully

Go beyond the listing photos. When you visit a home, look for signs of deferred maintenance: water stains on ceilings, evidence of foundation cracks, the age and condition of the HVAC system, water heater, and roof. These are the expenses that blindside new homeowners. Your inspection contingency (more on this below) is your safety net — use it.

💡 First-Timer Tip

Even if you fall in love with a home, visit it at multiple times of day and on different days of the week. A quiet Sunday afternoon can look very different from rush hour on Monday morning. Check the commute, the noise levels, and the neighborhood activity.

New Construction: A Hidden Gem in 2026

NAR reports that townhomes now account for about 18% of single-family construction — up from less than 10% a decade ago — specifically because builders are targeting first-time buyers who need more affordable entry points. If existing-home inventory is tight in your area, don't overlook new construction communities. You'll often get brand-new everything, builder warranties, and those attractive rate buydown incentives.

05. Making a Competitive Offer

Found the one? Here's how to structure an offer that protects your interests while being attractive enough to win.

Key Components of a Purchase Offer

1. Purchase Price

Your agent will pull recent comparable sales ("comps") to help you decide what to offer. In a balanced 2026 market, starting at or slightly below asking is often reasonable — unlike 2021, when you needed to go 5–15% over.

2. Earnest Money Deposit

Shows you're serious. Typically, 1–3% of the purchase price is held in escrow. You lose this if you back out without a valid contingency. You get it back if the deal falls through due to contingency issues.

3. Inspection Contingency

Gives you the right to have the home professionally inspected and to renegotiate or walk away based on findings. Never waive this on your first home purchase.

4. Financing Contingency

Protects you if your mortgage falls through for legitimate reasons. Allows you to get your earnest money back. Standard in most offers.

5. Appraisal Contingency

If the home appraises below the purchase price, this gives you options: renegotiate, make up the difference in cash, or walk away. Important protection given that some markets are still seeing seller-inflated prices.

6. Closing Timeline

Typically, 30–60 days after offer acceptance. You can offer a faster close (competitive) or request seller concessions to offset costs. Ask about seller credits toward closing costs — this is more common again in 2026.

💡 Negotiation in 2026

Don't be afraid to ask for things. NAR notes that the market is the most balanced it's been in almost a decade. Sellers still want to sell — they're just no longer holding all the cards. Asking for $5,000–$10,000 in closing cost credits, or a 2-year mortgage rate buydown from a builder, is entirely reasonable in today's environment.

06. From Accepted Offer to Closing Day

Offer accepted — congratulations. Now begins the 30–60 day closing process. It's busier than most first-timers expect.

The Closing Timeline at a Glance

💡 Critical Warning

Never wire money without independently verifying the wire instructions directly with your title company or escrow officer — call them using a number you find independently, not one in an email. Wire fraud targeting homebuyers is the fastest-growing form of financial fraud, and wired funds are nearly impossible to recover.

07. Which Mortgage Loan Is Right for You?

Not all mortgages are created equal, and the right loan depends on your credit, savings, and circumstances. Here's an overview of the main types available in 2026:

Per The Mortgage Reports, conforming (conventional) loans allow as little as 3% down with credit scores starting at 620, while FHA loans are even more lenient — sometimes approving buyers with scores as low as 580 and less-than-perfect credit histories. VA loans remain the single best deal in mortgage lending if you qualify: zero down payment, no PMI, and typically competitive rates.

08. Home Buying Glossary

The home-buying process comes with its own language. Here are the key terms you'll encounter:

Bottom Line

The 2026 housing market isn’t about rushing — it’s about positioning. Rates have eased, inventory is improving, and buyers finally have room to negotiate again, but success still comes down to preparation. The buyers who win this year won’t be the ones waiting for perfect conditions — they’ll be the ones who understand their numbers, shop smart, and make confident, informed decisions at every step.

If you take anything from this guide, let it be this: focus less on timing the market and more on being ready for it. When your finances are solid, your expectations are realistic, and your strategy is clear, buying a home stops being overwhelming — and starts becoming one of the smartest long-term moves you can make.